Case Study: How a Contractor With $460,000 in MCA Debt Recovered $9,385 a Week Through Reverse Consolidation

• A Florida construction company carrying 7 MCA positions and $460,000 in balances reduced its weekly payments from $21,845 to $12,460, a 43% cut.

• Every existing advance was paid through to the end of its term, with five of seven positions fully paid off within four months of funding.

• No settlement, no default, and no negotiation with the original funders was involved at any point.

Matthew Elling

Founder and CEO

Posted on

July 3, 2026

The Business at a Glance

Industry: Residential construction services

Location: Florida

Annual revenue: roughly $3.8 million

MCA positions: 7

Total original MCA funding: $782,000

Outstanding MCA balances at engagement: $460,000

Weekly MCA payments: $21,845

Monthly debt service: $87,380, roughly 30% of gross revenue

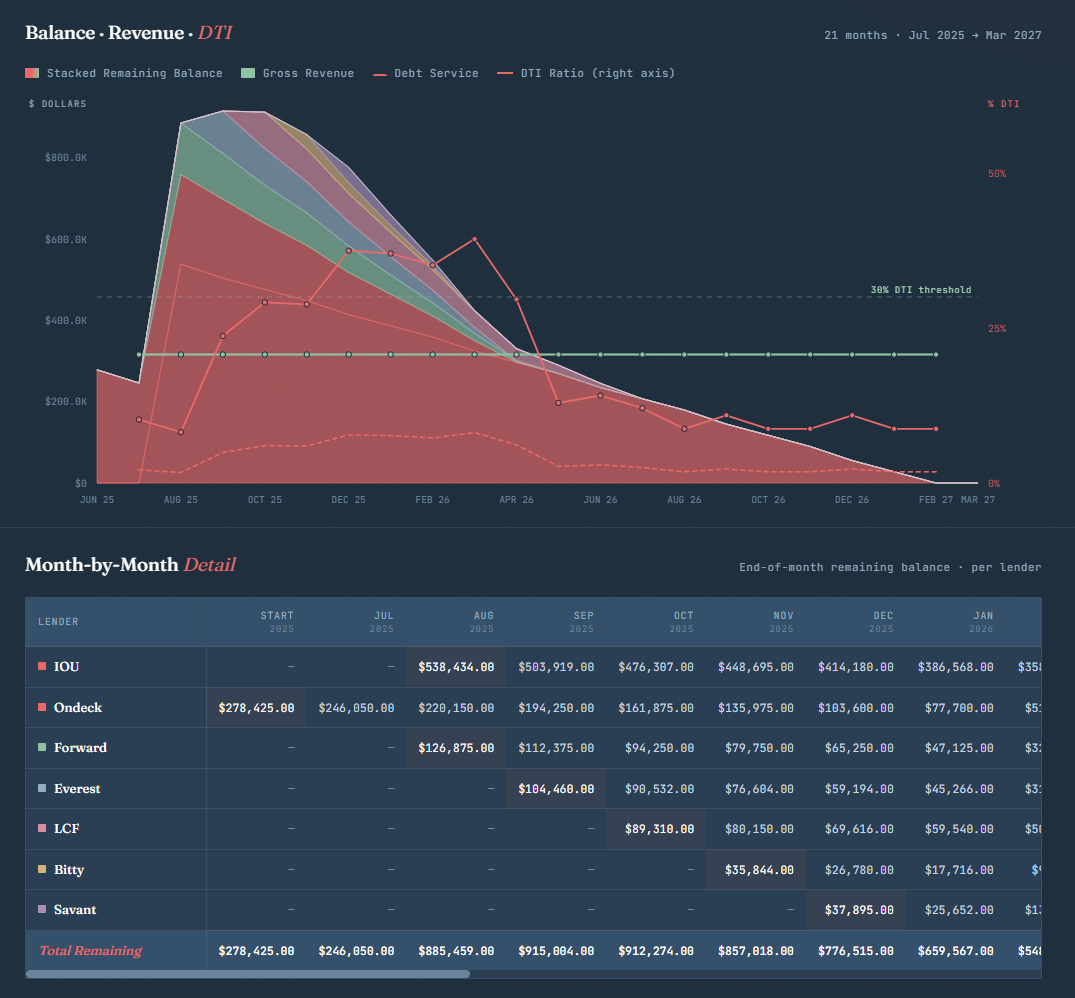

Seven positions stacked between July and December 2025. At its peak, the combined remaining balance topped $900,000 and debt service consumed nearly 40% of monthly revenue.

The Challenge: When the Bridge Becomes the Bottleneck

In early 2026, a Florida-based residential contractor contacted ReverseConsolidation.com carrying seven separate merchant cash advances with combined balances of roughly $460,000.

The advances made sense individually. Construction cash flow runs on a lag. You front labor and materials to start a job, then wait on draws and final payment. Each MCA bridged that gap. But each new advance added its own daily or weekly pull, and by late 2025 the stack had grown to seven positions drafting a combined $21,845 every week.

The tool that once bridged jobs was now blocking them. With $87,380 leaving the account every month, there was not enough working capital left to mobilize crews and buy materials for new projects. The company was turning down work it was fully capable of performing.

Revenue stayed strong the entire time. That is the part most people outside the MCA world miss. The problem was never sales. It was the payment velocity:

Payroll timing got harder every week

Vendor payments started slipping

Growth plans went on hold

Cash reserves drained between draws

Traditional financing was off the table because of the existing MCA exposure

The company was not in default. Not one missed payment. But the owner could read the direction of travel, and it pointed toward the same stacking cycle that is driving MCA defaults across the country: take an eighth advance to cover the seven, then a ninth to cover the eight.

What Did the Reverse Consolidation Actually Change?

After reviewing the company's cash flow, bank activity, and all seven outstanding positions, a reverse consolidation was structured around one principle: every existing MCA gets paid exactly as agreed, through to the end of its term.

There was no settlement. No negotiation. No modified agreements. The original funders were never contacted, because nothing about their agreements changed. Here is how the mechanics work: the reverse consolidation funds the company's account on a schedule that covers the existing MCA payments, while the company makes one smaller consolidated payment in their place.

The objectives were specific:

Keep all seven positions in good standing

Cut the weekly payment burden immediately

Free up operating cash flow from the first week

Break the renewal cycle so no eighth position was ever needed

Buy the business the time to stabilize on its own revenue

The Results: 43% Off the Weekly Payment, Every Position Paid in Full

The payoff sequence. Ondeck, Forward, Everest, Bitty, and Savant all reach zero by July 2026. Every position was paid through the end of its term. Nothing was settled, nothing defaulted.

Then the positions started falling off. That is the mechanical difference between a reverse consolidation and every other option on the table. MCAs are short-term instruments. Left alone, and actually paid, they die on their own schedule. Bitty was down to $412 by March 2026. Savant hit zero the following month. By July, five of the seven positions were paid in full, and the total stack had dropped from over $776,000 at year-end to just the two longest positions remaining.

The full 21-month timeline from this case, month by month.

The operational effects showed up within the first weeks after funding. Payroll stopped being a Thursday-night math problem. Crews mobilized on new jobs without waiting on receivables. And the pressure to take an eighth advance, the pressure that turns a manageable stack into an unmanageable one, was gone.

Is There a Ceiling on How Much MCA Debt Can Be Consolidated?

Many business owners assume that once MCA balances reach several hundred thousand dollars, the only remaining doors are default, settlement, or bankruptcy. All three of those doors lead somewhere worse than the current payment schedule.

This case says otherwise. There is no hard ceiling on the debt amount. A business carrying substantial MCA balances across many positions can still qualify, as long as the revenue is there to support a restructured payment. The qualifying question is not how much you owe. It is whether your cash flow can carry a payment 20% to 50% lighter than the one currently draining it.

Run Your Own Numbers

Every chart in this article came from the same payment savings calculator we use to model client scenarios, populated with this company's real figures. Plug in your own positions and revenue and you will see the same view: your projected payment reduction, your month-by-month payoff timeline, and the point where each position falls off.

If the numbers look like relief, the application takes about ten minutes. No credit check, no obligation, and your current funders are never contacted.

Results vary based on industry, revenue, existing obligations, and cash flow. Reverse consolidation is designed to improve cash flow management and is not a debt settlement or loan consolidation program.

CALCULATE YOUR PAYMENT SAVINGS

Enter Current Payments

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.

Why 2026 Could Be a Turning Point for Merchant Cash Advances and Small Business Debt Relief

The merchant cash advance industry continues to grow rapidly, but 2026 is shaping up to be a pivotal year for both MCA providers and the businesses that rely on them.

MCA Defaults Are Rising: Is the Merchant Cash Advance Industry Reaching a Breaking Point?

MCA defaults are climbing as rising costs push healthy businesses into the stacking cycle. Learn why merchants default and how a reverse consolidation lowers payments without defaulting.

Bankruptcy Attorneys Are Saying It Out Loud: MCA Debt Is Driving Small Business Insolvencies

Bankruptcy attorneys report MCA debt is driving small business insolvencies nationwide. 230+ filings in 2025, 21-deal bankruptcies, and a reverse consolidation exit ramp that closes once collections start.

Senate Pressure on SBA Sheds Light on the Merchant Cash Advance Industry

A Senate letter to the SBA is raising questions about whether tariff policies and MCA refinancing restrictions trapped small businesses in high-cost debt with no way out. Here's what it means for business owners managing merchant cash advances right now.

What Happens When You Default on an MCA — And Why You Have Less Time Than You Think

If you're behind on MCA payments or worried you're about to be, the legal cascade that follows default is faster and more aggressive than most business owners realize. This article walks through what actually happens after default, why the moves merchants instinctively make to slow the bleeding make it worse, and the restructuring window that closes once enforcement begins.

.svg)